How China-Taiwan Tensions Will Reshape Chemical Industry Strategy

Drawing from 30 authoritative industry sources, we’ve mapped how this geopolitical shift creates both vulnerabilities and competitive advantages through 2026. The leaders profiled inside are already implementing the response framework. Are you?

The 44% problem

When a single country controls nearly half of global chemical production capacity, you don’t just have a manufacturing hub – you have a looming strategic vulnerability.

China now accounts for 44% of global chemical production capacity and 46% of the sector’s capital investment [1]. This is more than a statistic; it’s a risk scenario that’s keeping many chemical industry strategy leaders awake at night. The connections between this manufacturing hub and global supply chains run deep through one of the most geopolitically contested regions on the planet — the Taiwan Strait.

What happens when China-Taiwan tensions threaten to upend the flow of critical materials? The answer is forming now, as forward-thinking industry leaders move toward reframing potential production disruptions into opportunities to capture competitive advantage.

5 signals chemical executives need to know

Multiple converging signals suggest we’re at an inflection point where strategic positioning will determine which companies merely survive and which ones thrive through this period of elevated geopolitical uncertainty.

- Raw material costs are projected to increase 5-10% in disruption scenarios, with production disruptions lasting weeks to months [2]

- About 40% of companies are increasing US sourcing, and 32% are employing dual supply chains to reduce geopolitical risks [3]

- Nearly 8 in 10 businesses are reducing dependence on China by diversifying to other emerging markets, with 63% engaging in “friend-shoring” [4]

- The chemicals sector in Europe has been hit by tariff threats, leading to demand uncertainty and production adjustments [5]

- China’s strategic positioning continues to grow, with BASF planning a €10 billion integrated base in Zhanjiang focused on bio-based polymers and flame-retardant materials [6]

These signals are telling a story of an industry in transition; moving from an era of efficiency-first globalization toward a model that prioritizes reduction of supply chain vulnerability alongside more traditional cost considerations.

Where supply chains are most vulnerable

The chemical industry’s dependence on China creates vulnerabilities that extend far beyond direct sourcing relationships:

Dependency metrics to monitor

- Production concentration: China’s dominant role means even companies without direct Chinese suppliers face significant indirect exposure [7]

- Raw material access: Trust in China’s political and economic stability has declined, with the EU particularly vulnerable as it sources rare earth magnets almost exclusively from China [8]

- Downstream effects: Disruptions would cascade into industries such as agriculture, electronics, and pharmaceuticals, causing production slowdowns and ballooning costs [9]

Geographic vulnerability analysis

Recent reports from J.S. Held (February 2025) and the Middle East Insurance Review (March 2025) highlight how organizations face higher risks of acute supply chain failure in 2025 due to geographic concentration [10, 11]. This vulnerability is particularly pronounced in:

- North America (highest dependency on Chinese chemical imports)

- Europe (especially vulnerable to rare earth and catalyst shortages)

- South America (limited alternative sourcing options)

- Middle East (moderate vulnerability with growing local production)

- Africa (relatively less integrated with Chinese supply chains)

The vulnerability ranking reveals a counterintuitive reality: geographic distance from the potential conflict zone doesn’t necessarily reduce economic exposure.

In fact, North American chemical companies often face higher risk due to their deep integration with specialized Chinese suppliers and limited domestic alternatives for certain high-value precursors and catalysts.

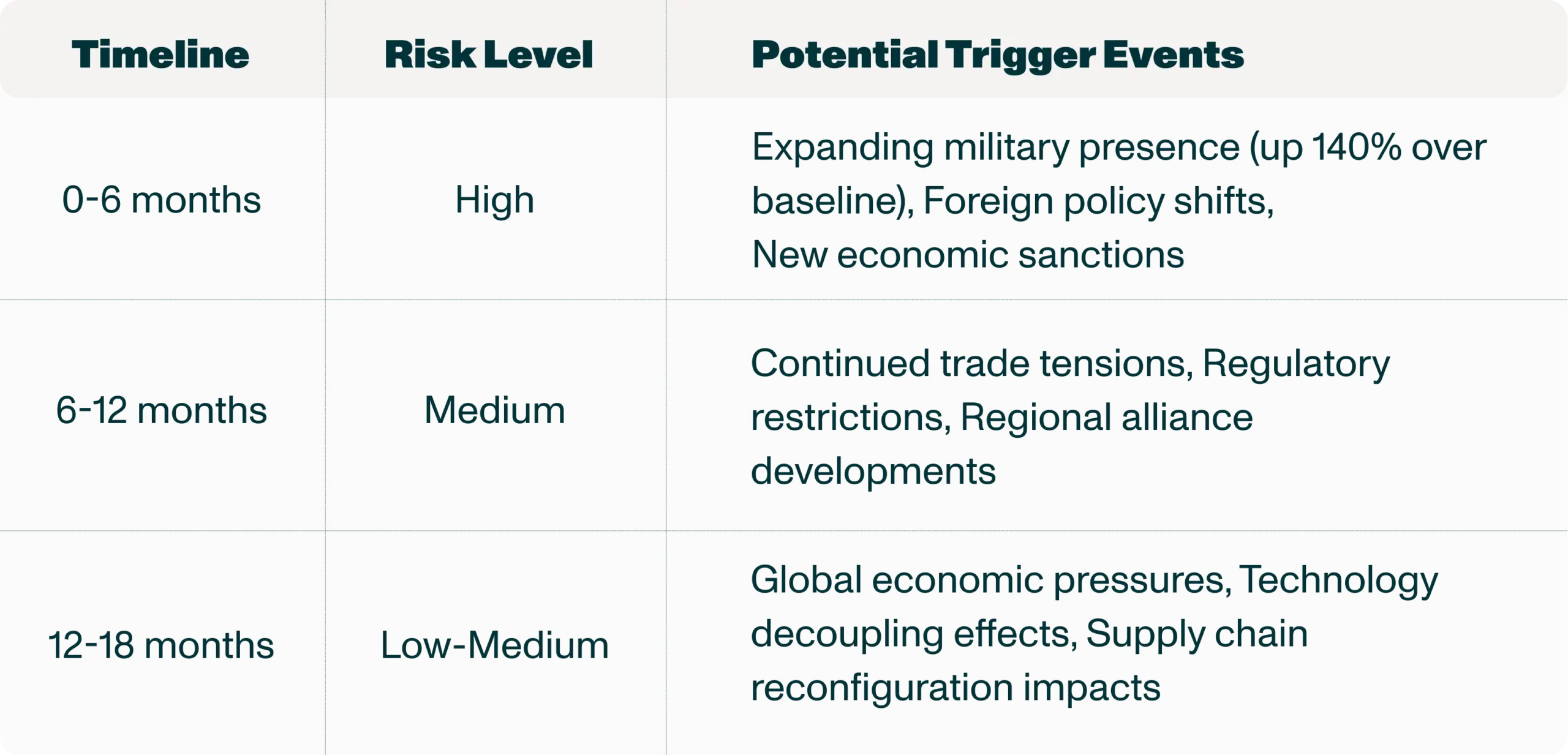

The 18-month action window

Intelligence analysis from various 2025 sources suggest varying probability levels for escalation:

This timeline isn’t theoretical – it’s based on current patterns observed across global markets. Geopolitical instability has become a more significant driver of risks to trade according to Business Insurance (March 2025) [12], creating both immediate threats and strategic opportunities for risk mitigation.

How industry leaders are responding

Leaders in the chemical industry are implementing sophisticated strategies to manage the evolving situation:

BASF

- China investment: Planning a €10 billion integrated base in Zhanjiang focused on bio-based polymers and flame-retardant materials, showing continued commitment to the Chinese market while pursuing diversification elsewhere [6]

- Local production strategy: Focusing on R&D and manufacturing tailored specifically for the Chinese market to maintain competitiveness regardless of geopolitical developments [6]

Dow

- Strategic caution: Taking a measured approach by delaying projects and reviewing European assets following tariff threats and market volatility [5]

- Supply chain resilience: Implementing digital strategies and advanced analytics to increase visibility across global operations [13]

Chinese chemical enterprises

- Market diversification: Chinese companies are expanding beyond single-market dependency, with stable operations in Europe, the Middle East, and Southeast Asia, while also exploring South America, Africa, Mongolia, and Russia [14, 15]

- “US risk” mitigation: Deliberately reducing US business exposure in response to trade tensions, with nearly half of surveyed Chinese foreign trade enterprises planning decreased US engagement [16]

Why decoupling is a two-way street

A critical pattern emerges when analyzing recent data: chemical supply chains are fragmenting along geopolitical lines, creating what analysts call a “decoupling dynamic.” This is not a one-sided process but rather two complementary trends occurring simultaneously:

- Western companies pulling back from China: Approximately 40% of Western and global companies are increasing US sourcing and 32% are employing dual supply chains to reduce China exposure [3]

- Chinese companies pulling back from the US: Nearly half of surveyed Chinese foreign trade enterprises are actively planning to decrease their US business engagement [16]

This mirror-image response reveals a fundamental restructuring of global supply chains rather than simply a temporary adjustment. As both sides reduce interdependence simultaneously, new regional supply hubs are emerging to fill gaps – particularly in Southeast Asia, India, and Mexico.

For chemical industry executives, this bidirectional decoupling creates both immediate challenges and strategic opportunities:

- Supply gap recognition: Identifying where mutual withdrawal creates critical material or capacity shortages

- New supplier development: Building relationships with emerging producers in “neutral” territories

- Regional strategy differentiation: Developing distinct approaches for increasingly separated economic spheres

Companies that recognize this is not simply “de-risking China” but rather a fundamental global realignment will be better positioned to navigate the emerging multipolar chemical market landscape.

Specialty chemicals exposure: Impact analysis by sector

The volatility in European markets due to tariff threats is already affecting specialty chemical sectors according to ICIS (April 2025) [5]:

Agricultural chemicals & crop protection

- Immediate disruption risks: Tariff uncertainties and market volatility are negatively impacting demand predictability [5]

- Real-world example: Recent protests in Pakistan against a canal project have disrupted transportation and caused raw materials shortages, demonstrating how quickly regional tensions can affect global supply [17]

- Strategic contradiction: While disruption risks are pushing toward localization, specialized agricultural chemistry often requires economies of scale that only China-sized production can efficiently deliver – creating a strategic dilemma for western agricultural chemical producers

Polymers & plastics

- Immediate disruption risks: European market volatility due to tariff threats is directly impacting activity, with companies avoiding long-term orders [5]

- Strategic implications: Paint and coatings industry manufacturers are already turning to local supply chains in response to global uncertainties, according to European Coatings (April 2025) [18]

Industrial chemicals

- Vulnerability Indicators: Geopolitical tensions and currency volatility are creating market instability and demand uncertainty [5, 19]

- Adaptation Patterns: Companies are increasingly implementing net zero plans and adopting AI technologies to navigate economic and geopolitical complexities [20]

Paints & coatings

- Current disruptions: The industry is already feeling the impact of global uncertainties, with manufacturers turning to local supply chains [18]

- Future trajectory: Industry analysis shows a shift toward local sourcing and sustainability focus could restructure the entire supply chain [18]

Strategic response framework for chemical executives

Based on current market intelligence and emerging best practices, chemical executives should implement a staged response that acknowledges a key reality: there is no “one-size-fits-all” approach to geopolitical risk in the chemical industry. Different subsectors, company sizes, and geographic focuses require tailored risk mitigation strategies:

Monitoring phase (current)

- Map complete supply chain: Comprehensive mapping and detailed analysis of current infrastructure and supplier dependencies, as recommended by Kearney (November 2024) [21]

- Assess tariff impacts: Evaluate implications of potential trade policy changes involving China, Mexico, and Canada, as advised by KPMG (April 2025) [22]

- Track early warnings: Monitor military movements, diplomatic signals, trade patterns, shipping metrics, and supplier behavior changes [23]

Early preparation phase (0-3 months)

- Diversify sourcing: Begin expanding supplier networks geographically to mitigate country-specific risks [24]

- Stress-test supply chains: Run disruption scenarios to identify critical vulnerabilities, as recommended by Die Presse (November 2024) [25]

- Update contract provisions: Review force majeure clauses and risk allocation provisions to clarify responsibilities during disruptions [26]

Active mitigation phase (3-9 months)

- Implement friend-shoring: Shift critical sourcing to allied nations, a strategy now employed by 36% of executives worldwide according to Supply & Demand Chain Executive (November 2024) [27]

- Invest in technology: Deploy advanced analytics and AI-driven supply chain visibility tools, as modeled by Nissan according to Industry Insights (April 2025) [28]

- Build strategic reserves: Increase inventory of critical materials with high China exposure, especially catalysts and precursors [29]

Crisis response phase (if triggered)

- Activate command center: Establish daily coordination structure with clear decision authorities [30]

- Implement allocation protocols: Deploy pre-determined production prioritization frameworks [30]

- Execute communication plan: Maintain transparency with customers and stakeholders without creating panic [30]

Moving forward

The unfolding China-Taiwan dynamics are creating a watershed moment for the chemical industry. This is more than a geopolitical situation to monitor; it’s a strategic inflection point that will separate market leaders from followers over the next 18-36 months.

Those who gain competitive advantage will be companies that transform these insights into action:

- China’s dominance in chemical production creates systemic risks that extend throughout global supply chains

- Current geopolitical signals suggest a high-risk window in the next 6 months that demands immediate preparation

- Leading companies are pursuing multi-faceted risk-mitigation strategies: geographic diversification, friend-shoring, technology investment, and local production

- Industry sectors are responding differently, with paints and polymers moving fastest toward supply chain reconfiguration

- Effective response requires a progressive approach from monitoring through preparation to active mitigation

- Companies that implement strategic responses now will gain competitive advantage as market conditions evolve

When properly prepared, disruption creates openings for innovative players to capture market share, strengthen customer relationships, and build more resilient business models. The chemical executives who recognize this dual nature of the current situation—both threat and opportunity intertwined—will be those who emerge stronger on the other side.

How we built this

We (the marketing team) asked VAL, our AI research assistant, to analyze potential impacts of China-Taiwan tensions on the global chemical industry.

VAL immediately got to work:

- Scanning 200,000+ premium global sources

- Identifying industry-specific vulnerability patterns

- Quantifying potential financial impacts

- Assessing competitive positioning of industry leaders

- Developing a practical response framework

Total time from question to comprehensive report? Under an hour. Which begs the question: what could your team do with this kind of on-demand analysis at their fingertips?